Market Update: 8 July 2021

There’s been much talk about the upcoming GBTC share unlocks which begin in earnest next week (Chart 1). We’ve discussed Grayscale and GBTC previously but would like to go into greater detail in the second part of this note.

GBTC is still primarily a retail vehicle, where the known public institutional holders account for 12.21% of the total outstanding shares — of which 3AC is the largest shareholder at 5.62%, holding a very auspicious 38,888,888 shares (Chart 2).

The upcoming unlocks are for institutional holders who subscribed directly to GBTC 6 months ago — and this batch consists of all the new Q1/2021 positions, largely ARK’s last tranche (Chart 3).

To state clearly — We dont expect these unlocks on its own to have significant impact on the overall market outside of GBTC itself. Most of the large institutional positions who had subscribed in-kind before have already been unlocked earlier, and they have held off selling at the current discounted price. Moreover we know a large chunk of ARK’s stake is for a variety of their current ETFs like their Next Generation Internet ETF.

The fact that the market is so focussed on something like this just shows the lack of real catalysts or market moving events right now, and strengthens our conviction in our short 30/40k strangle view — which we like even more now. We expect volatility to remain under pressure until mid-late Aug and for 1m implied vol to return to the long-term 50–60% range, where we will flip to vol buyers again (Chart 4).

Right now our trading plan follows the 2018 BTC Analog — where we expect a dampened trading environment from here to Aug (short vol), followed by a rally possibly on the back of the EIP-1559 mainnet implementation (long spot, long calls), and then the larger Q4 Wave 5 selloff on the Fed’s taper (sell spot, buy downside risk reversals). (Chart 5)

PART II: GBTC mechanics

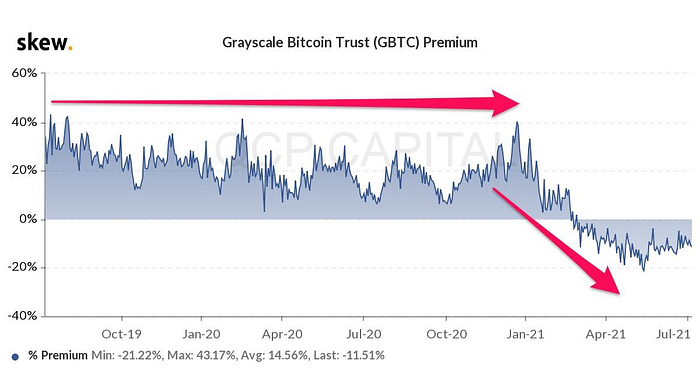

- This will be the last batch of unlocks as GBTC went into discount for the first time ever in Q2 this year — meaning new interest would simply buy in the open market, as compared to the prior dynamic of subscribing in kind at par, holding it over the 6 months (previously 1 year) lockup, and then selling at the average 20–30% premium that had persisted very consistently over the prior years (Chart 6).

2. It was the last unlock in late Q1 this year that drove GBTC into discount to spot price — large names like Blockfi were selling (likely in response to the launch of the Purpose Bitcoin ETF — Chart 7).

3. Since then we have not seen much selling interest from large holders who have already had their shares unlocked, probably choosing to wait for GBTC to trade at a premium again. Admittedly most of them would not have expected it to persist in such a large discount for so long, having expected arbitrageurs to come in and close the NAV gap.

4. We have always maintained that with redemptions continuing to be suspended, there remains no mechanism for GBTC to go back to par and it could persist in discount for a long time.

5. Outside of that, selling/buying of GBTC in the open market would just lead to wider/narrow discounts over NAV.

6. In fact as BTC matures, and institutions get more comfortable holding physical coin, they will see little reason to pay Grayscale the very steep 2% annual management fees. Furthermore in the unlikely event a BTC ETF is approved in the US it would mean the death keel for GBTC in its current closed-end fund/trust structure.

7. GBTC was essentially a “long-end of the BTC curve” play, where one could subscribe with physical BTC at par value and capture the GBTC price premium after the lock-up period. A tonne of leverage was used to maximise profits on this premium of the ‘terminal forward’:

i. Borrow BTC and subscribe at par and receive GBTC in 6 months. Profit is earned if the premiumover spot after 6 months is higher than the interest rate.

ii. Borrow USD to make a double spread by buying physical BTC and short the perpetual swaps or futures (earn 1st spread), then use the physical BTC purchased to subscribe to GBTC to earn the premium after 6 months (earn 2nd spread).

8. Besides BTC holders who subscribe with their own BTC & later choose to take profit on said BTC by selling their GBTC shares in the open market for USD; every other leverage GBTC trade would involve using the USD proceeds from selling GBTC shares at the end to buy back spot and cover the BTC short again.

9. So does this mean GBTC unlocks are bullish spot? Initially yes — and with the persistent premium over NAV before it led to a positive bullish cycle for BTC whereby Grayscale without redemptions holds onto all the BTC subscribed with them, while institutions doing this trade had to keep buying spot after selling their GBTC shares for USD.

11. However this bullish cycle was contingent on the premiums persisting — which would attract new in-kind subscriptions, 6 months lock-up, sell GBTC shares buy back spot, rinse & repeat.

12. In a discount phase however, it means not only no new subscriptions, but those who are interested in owning BTC can buy GBTC at discount in the open market — which negates any bullish new capital impact on spot.

13. Which is essentially why backwardation is negative in the BTC near-end forward market, and why we dont expect a bull cycle to return until either an ETF is approved or GBTC goes back into premium.

14. So what can Grayscale do to get GBTC back into premium? An immediate move would be returning capital to shareholders through share buybacks, and they have already been doing so this year — having bought roughly $200m worth, with up to $750m authorised by DCG using Grayscale’s cash on hand.

15. Converting to an ETF would be the most obvious future solution, but thats entirely out of their hands, and into the still-skeptical hands of the SEC. An ETF structure with more frequent & accessible subscription/redemptions would certainly result in their share price trading much closer to par.

16. However, the flip-side to that is Grayscale themselves will be forgoing the very juicy 2% management fees they currently collect — which at the current AUM of $22bn from 651k BTC amounts to a cool $440m a year. Also with an ETF — crypto institutions who have for years been profiting off these risk-free arbitrages would have to kiss them goodbye for good, although in the current discount regime these holders would no doubt be happy to get out at par.

17. A lot of the lending desks paying high borrow rates have been using arbitrage strategies such as this GBTC premium arb as their base, and we would expect to see lending rates come down as a whole, and the attractiveness of the crypto space as a high base yield asset class lose its shine.

(incidentally a key reason why we are so focused on the options market which will continue to offer extremely attractive 100+% annualized yields, even as yields everywhere else normalize to single digits as we are seeing now)

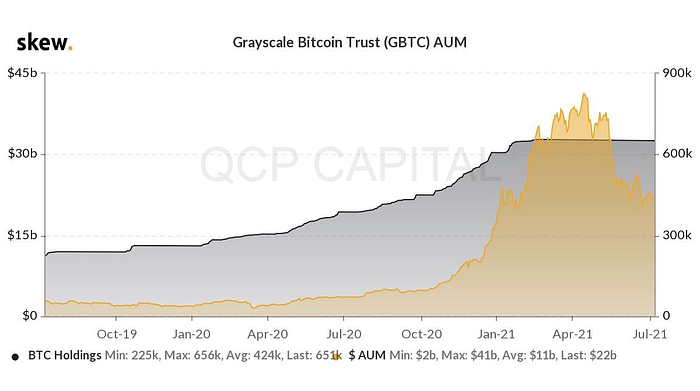

18. Of course, if the discount gets steeper then a possible syndicated takeover offer could come — but in the event of this we expect a very negative BTC price reaction. Don’t forget GBTC is by far the largest public holders of BTC — 651k now which is a mile more than the next largest holders (Chart 8).

19. Restarting redemptions would certainly close the discount to NAV — but the cost to BTC price itself would be great, and any buyer looking to takeover would also no doubt be cognisant of that. Liquidating such a massive pool of BTC will always be the challenge for them, and any sign of selling from GBTC would crash the BTC market in the near-term. As a result thus far they have only been selling amounts necessary to cover fees and miscellaneous expenses — just 5k BTC from the peak of 656k holdings since Feb (Chart 9).

20. In the meantime, with funding costs low it enables holders of GBTC shares to wait out the return to premium rather than cutting loss here. But we do expect this to happen at some point as the par level to NAV has provided strong support for arbitrageurs in the prior years before, it will be a ceiling going forward now. with new subscriptions remaining close to zero.